Sanjay Rajan is Director of Digital at First Tech Federal Credit Union. He and his team are passionate about design-driven, scalable products that humanize digital.

Digital innovation is changing the financial industry at break-neck pace.

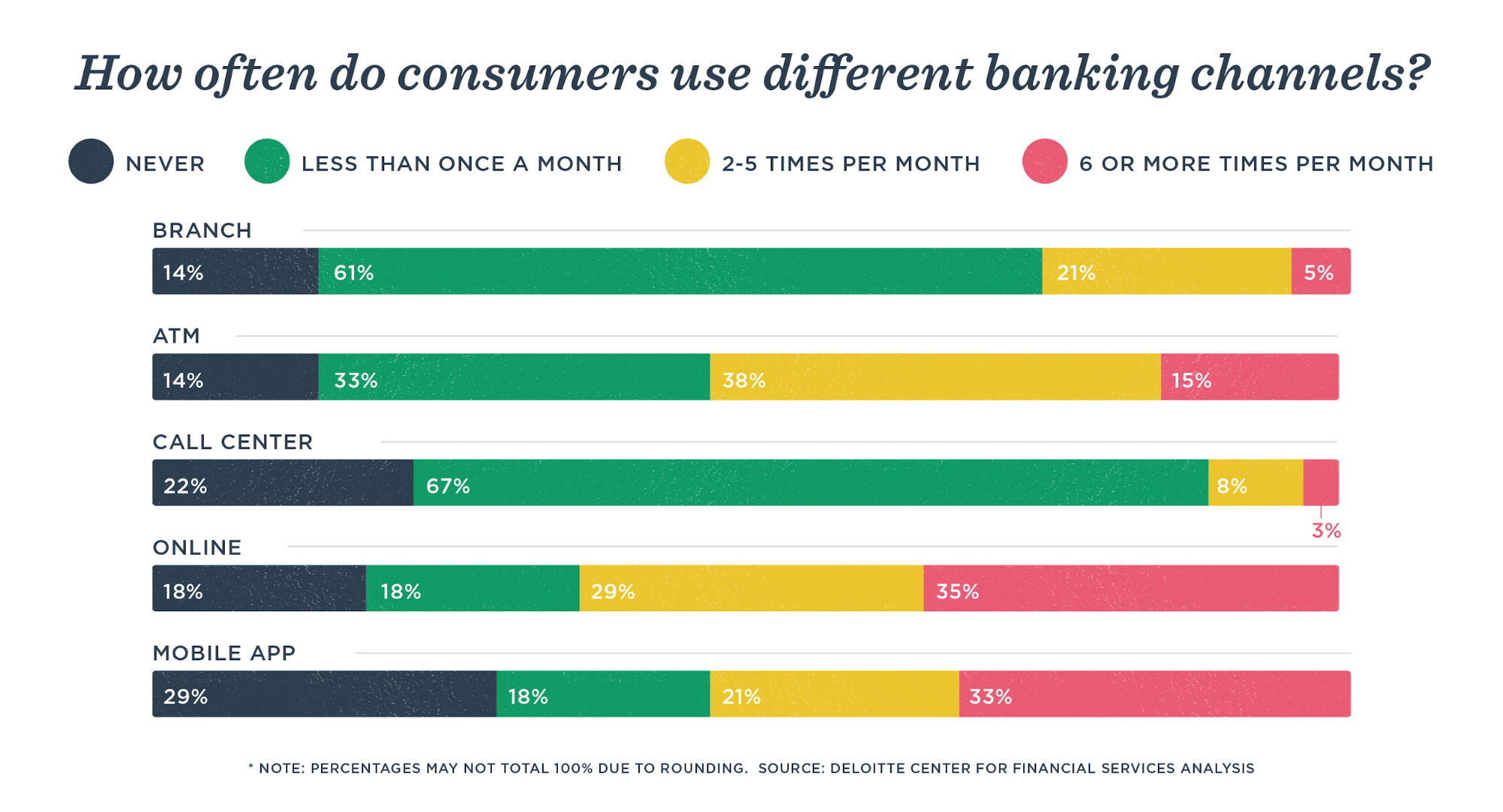

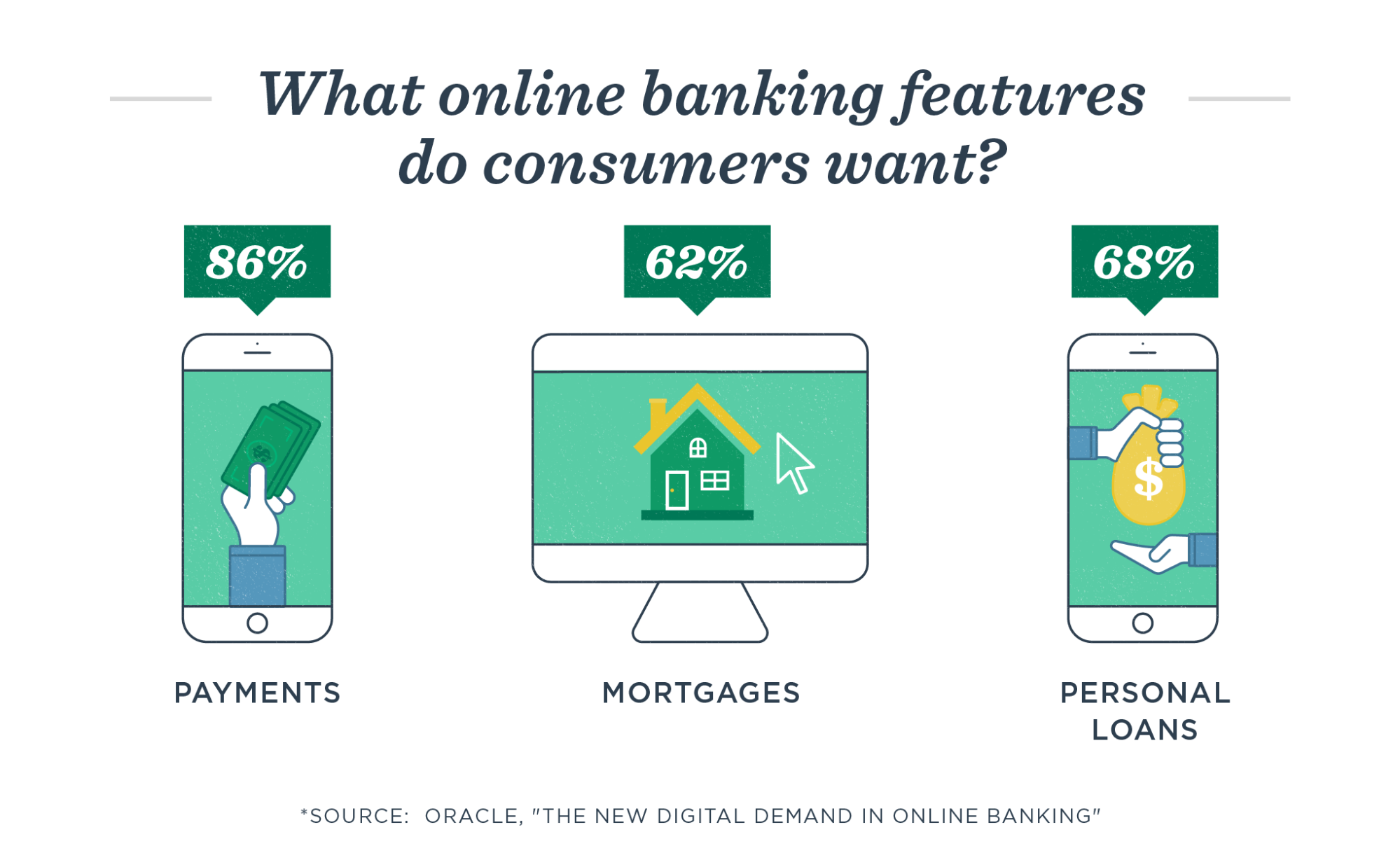

According to a recent study by Deloitte, 84% of consumers use digital banking, with 72% accessing their primary account via a mobile channel.

Meanwhile, banks are hurrying to catch up. In fact, 73% of financial institutions increased their investment in online channels over the last year.

A banking arms race.

As consumers move their financial lives online, it’s no longer enough merely to offer desired features and functionalities. Today, banks live or die based on the overall quality of their customer experience (CX). Often that hinges on how well a company’s different channels and services are woven together.

Put another way: attractive features, intuitive interfaces, and self-populating form fields are essential for a good CX—but at this point, they’re table stakes. What today’s consumers expect is the ability to move across platforms seamlessly, without having to repeat a keystroke or revisit a screen. It’s just as important to them as the raw functionality.

It’s not a multi-channel approach. It’s the omnichannel experience that has become the gold standard in banking CX. To create it, banks and credit unions must follow these four steps:

Map the customer journey.

Eliminate silos.

Develop a build vs. buy strategy.

Look beyond the tech.

To demonstrate the importance of omnichannel, let’s take a look at an increasingly typical onboarding journey. (article continues below)

Could you onboard Emma?

Emma Knowles is 25 years old.

She’s a senior programmer with Flexport, a tech startup in San Francisco. She’s talented and driven—and insanely busy. Since she started with Flexport three years ago, she’s been promoted twice. Now she needs a loan so she can go back to school for her master’s in software engineering.

Over lunch one day, she visits a bank branch to start her loan application. But it’s taking longer than she expected, and she has to run to a meeting. So she dials into the bank’s call center on her walk back to the office. The rep pulls up her information and resumes filling out the form with her.

When she gets back to the office, she has to hang up. Her rep emails her a link to the online version of the application. Later, during a meeting, she pulls it up on her phone and fills out a few more fields. But she doesn’t get to finish it until that night after she gets home from work. There she finally has time to sit down at her computer and submit the application.

The new normal.

Emma’s journey is maddening for many traditional financial institutions. In the course of filling out a single form, she has moved across four channels: in-person, call center, mobile, and web. Why can’t she just sit down at a computer like a normal person?

But that’s the point. Increasingly, Emma is the norm.

She constantly moves across channels and devices. She doesn’t shop for one-off products. She wants to form relationships with companies that understand her lifestyle, values and goals. She isn’t rich, but she will be soon.

Emma is the money of tomorrow, and she needs a primary financial institution today. If you can follow her through her crazy day and get her to click “submit application,” then you could end up keeping her as a customer for the next 30 years.

If not, she’ll get frustrated and delete your app. You won’t get another chance with her. (article continues below)

Finding ROI in CX.

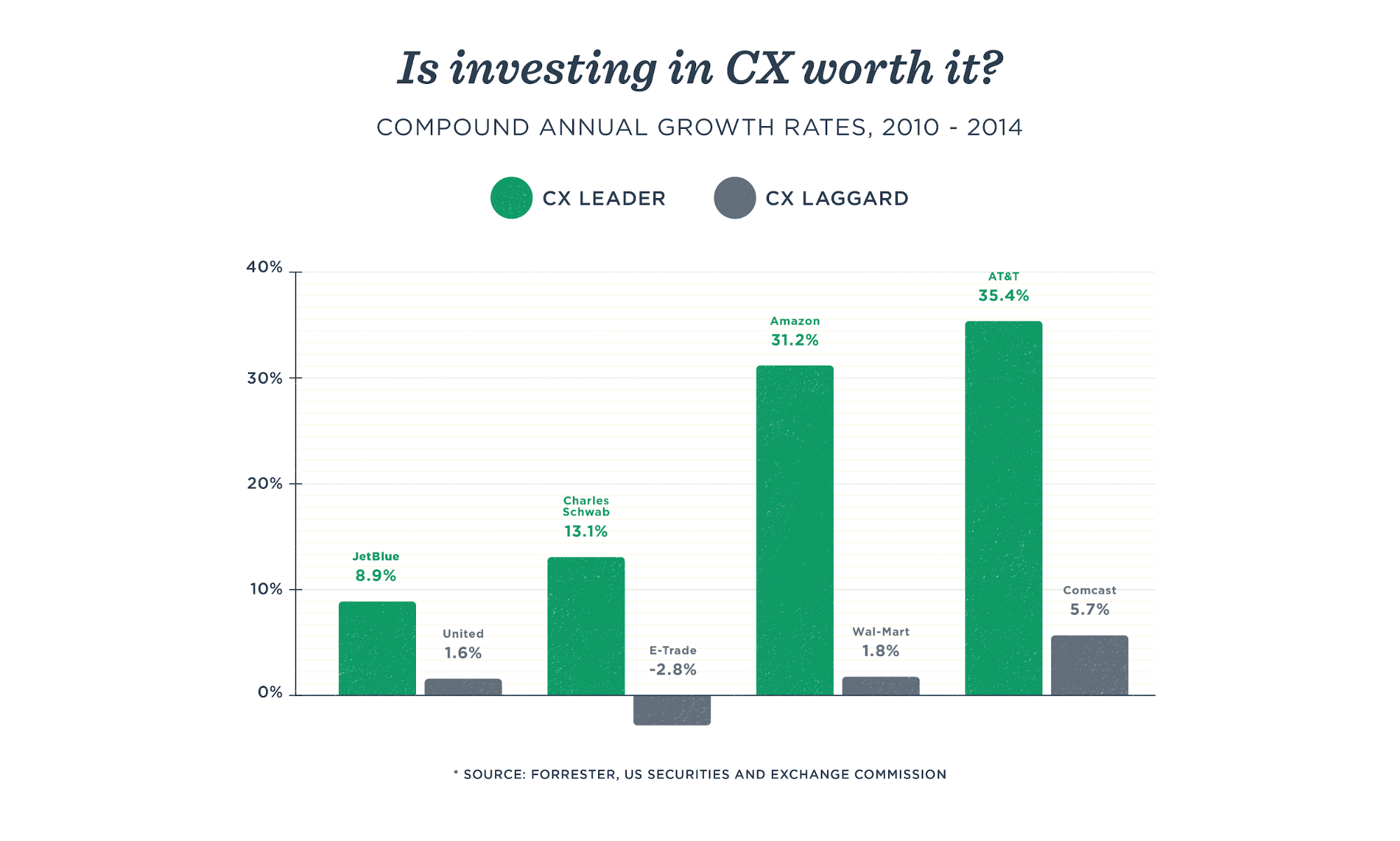

Investing in omnichannel is a lot of work, but it’s worth it. In fact, 70% of consumers say they consider a consistent experience across channels to be “extremely” or “very” important in selecting their primary bank.

In addition, companies that invest in excellent CX earn more revenue and grow faster than competitors who don’t. Compare the compound annual growth rates of Charles Schwab (13.1%) vs. eTrade (-2.8%), or Amazon (31.2%) vs. Walmart (1.8%).

And consider the alternative—not living up to customers’ expectations. Among customers who abandon organizations they do business with, 67% leave because of a bad experience. In fact, 30% say they will leave a brand they love after just one bad experience.

According to the recent study by Deloitte: “Companies that deliver a better CX tend to retain more of their customers, get more incremental purchases from their customers, and attract more new customers through positive word of mouth.”

Developing an omnichannel experience may seem daunting, but it doesn’t have to be. The technology is available, the API economy is expanding, and talented third-party providers are entering the digital ecosystem almost daily.

1. Map your customer’s journey.

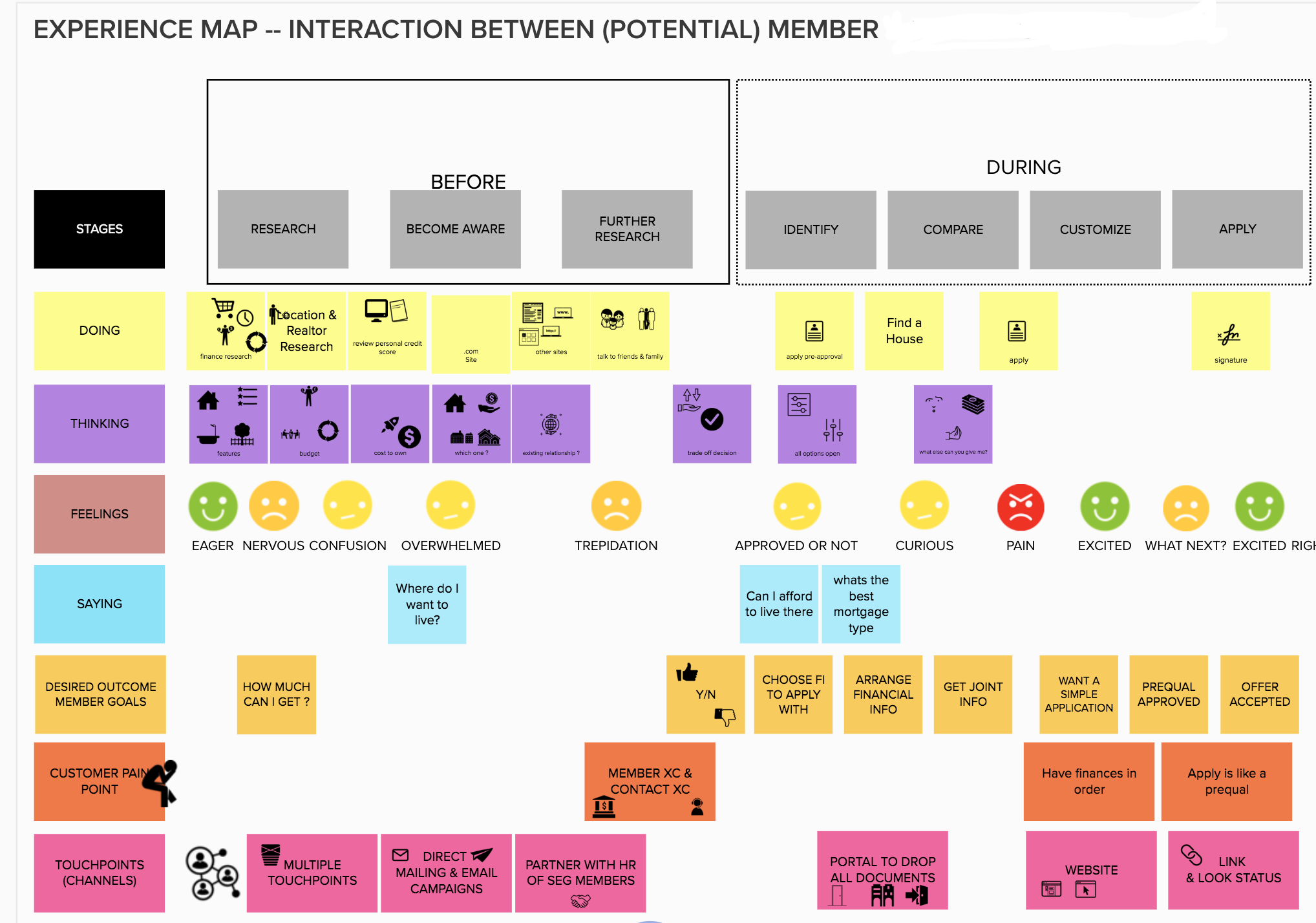

The first step is figuring out where to start and which channels to prioritize. To do that, you need an experience map.

An experience map is a visual representation of every interaction your customers have with you—from the moment they first see one of your ads or hear your name, through onboarding, to customer service and deepening engagement. It’s a great way to identify:

Customer pain points.

Where prospects are falling out of your funnel.

Moments of inconsistency from a brand perspective.

Opportunities for growth and scale.

I lead Omnichannel at First Tech Federal Credit Union. When we built our experience maps (see the image at the bottom of this section), we began by identifying several different primary journeys our customers take. Each had a different starting point and individual milestones. But, broadly speaking, each moved through four stages: inquiry→ onboarding→ satisfaction→ consideration of additional products.

The best thing about experience maps is that they often yield clear priorities about where to focus your development resources.

For example, do most daily visitors check their account balances? Then make it easy for them to get there directly from any channel or entry point. Is there a certain loan application screen where people give up and phone your call center? Mapping helps you identify that screen so you can fix it. (article continues below)

Sample experience map courtesy of First Tech Federal Credit Union

2. Eliminate silos.

Often, different products and channels are managed by separate teams within a company. Each team has their own goals and KPIs and views customers through a different, narrow lens. That might make sense from a business operations perspective, but it gets in the way of building a seamless omnichannel experience.

Suppose a customer calls to renegotiate the terms of a personal loan because they are experiencing financial hardship. You don’t want them to receive a direct mailer the next week encouraging them to take advantage of low mortgage rates.

Imagine how you might feel in that situation. You would frown, crumple the mailer, and toss it in the trash. Now think: is that how I want people reacting to my brand?

Like many financial institutions, First Tech had silos when we started building omnichannel. (And honestly, we still wrestle with this challenge). Many silos centered around different database systems and our employees’ understandable desire to protect sensitive customer data. Among product teams, we struggled with a sense of competitiveness and belief by each team that its product was the most important.

But that’s the thing. Omnichannel doesn’t work when silos exist. So start getting people on board:

Begin with senior leaders and work your way down

Prepare a formal presentation; approach it as a roadshow

Bring data about how omnichannel drives revenue and engagement

Offer concrete recommendations on how to restructure teams and KPIs

3. Develop a build vs. buy strategy.

Building out omnichannel is a lot of work. From the word go, many banks will need to weave together at least five channels:

Web 💻

Mobile 📱

In-person 💁

Call center ☎️

ATM 💸

From there, it only gets more nuanced. Do we need a mobile app? A chatbot? Voice recognition? How about a live customer service agent available via chat? Have we thought about social media?

Those questions are further complicated by the fact that most banks don’t have the internal development resources to build everything they need. The good news is that the marketplace is rife with great white-label options. Chances are you’ll end up building some functions in-house and contracting with outside vendors for others.

What should you build and what should you buy? Of course, it’s possible to make these decisions on an ad hoc basis. It “feels” like we should build our own payments product, whereas it “feels” like we can afford to buy a white-label messaging functionality for our website. But it’s much better if these decisions are driven by an overarching strategy.

At my company, we believe our competitive advantage lies in our customer experience, so we prioritize things that the customer directly touches. Our hypothesis is that customers choose us because they love working with us—both digitally and in person. For that reason, we build the front-end systems that create excellent CX. We want the most control over those things.

By contrast, we buy best-in-breed back-end systems that are invisible to the customer. That’s our build vs. buy strategy. What’s yours? (article continues below)

4. Look beyond the tech.

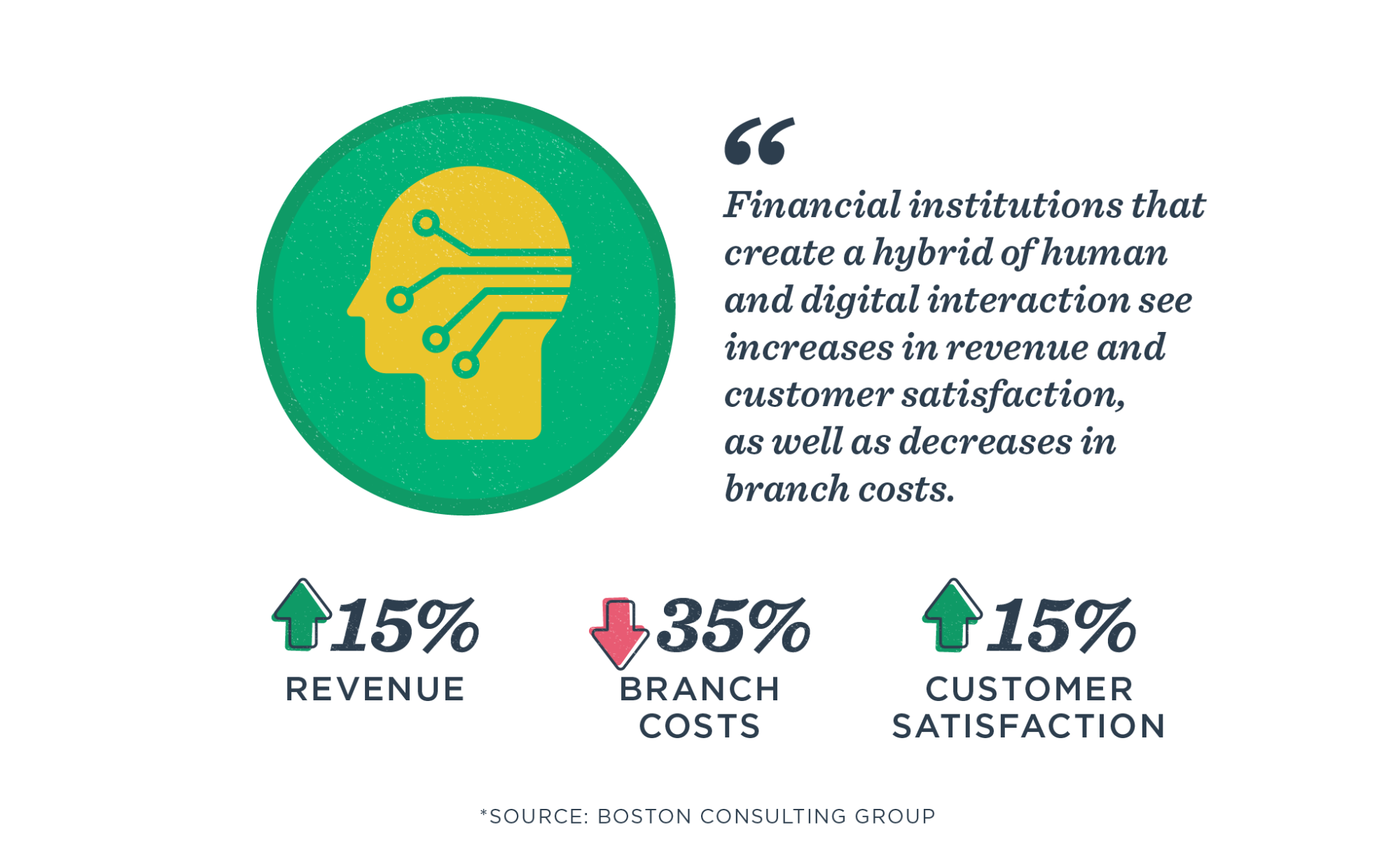

I’ve heard some in our industry say that branches will soon be obsolete.

Really? According to a 2019 study by Accenture, almost 70% of customers said they favored face-to-face interaction with their banks. Three out of four said they wanted their banks to provide a hybrid of digital and in-person services.

One takeaway from these and other data points: the branch isn’t going anywhere—at least not anytime soon.

The bigger story here is that you shouldn’t be so focused on the digital aspects of omnichannel that you neglect the human element. If people are getting stuck on a certain page of your loan application, the problem isn’t necessarily that they don’t know how to upload the required documents. It could be that they’re scared. Loans can be kinda scary.

In these moments, it helps to talk to another human. For this reason, you should take a hard look at your internal systems. Call your branches and call centers to ensure they can quickly retrieve and manipulate customer data. Even more important, make sure that the way they are communicating with customers is consistent with your brand.

The good news is that you will be rewarded for your labors. According to research from BCG, financial institutions that create an effective hybrid of human and digital experiences can see up to a 15% increase in revenue, a 35% reduction in branch costs, and a 15% increase in customer satisfaction. (article continues below).

A process of continual improvement.

Here’s the hard truth about omnichannel: you’ll never really be done developing it. Customer preferences will continue to change, as will technology.

And that’s good—because change is good. At First Tech, we recently launched the second iteration of our omnichannel experience, “Omnichannel 2.0.” It’s a marked improvement over the first version, thanks in large part to the lessons we learned mapping customer journeys and monitoring their experiences.

We’re already seeing the benefits. In the initial weeks after launch, we’ve seen our overall application completion rate increase to 65%, compared with an industry norm of 20%.

Are you ready to start building CX at your company? Before you start, consider these questions:

What are the needs and expectations of your customers? What will it take to do this research and build a journey map?

How easy/difficult will it be to secure executive buy-in from the C Suite? (This is critical).

Who in your organization could quickly grasp your vision and help you break through the silos?

What is your strategy for build vs. buy? Do you have the necessary resources in terms of both money and staff time?

Does your company have the stamina to endure a long, multi-phase project that will touch virtually every department?

Sanjay Rajan is Director of Digital at First Tech Federal Credit Union. He and his team are passionate about design-driven, scalable products that humanize digital.